October 21, 2015

Last Saturday, at 5:52AM, flight US1939, operated with an Airbus A321, landed at Philadelphia International Airport arriving from San Francisco. This would be the last flight flown with a US Airways flight number, an airline that traces its history back to 1939 (hence the flight number) as All American Aviation, founded by member of the Du Pont family.

This last flight was just another step in a merger process with American Airlines that was approved by the Department of Justice in late 2013. American Airlines is the lasting brand, but the merger was essentially a takeover of American by US Airways. The same happened with US Airways’s last merger, with America West in 2005. At the time, America West took over the then-bankrupt US Airways, but the more recognizable US Airways brand remained. Both airlines can claim heritage to more than a dozen airlines, including TWA and Reno Air on the American side and America West, Pacific Southwest, Piedmont, Mohawk, and Trump Shuttle on the US Airways side.

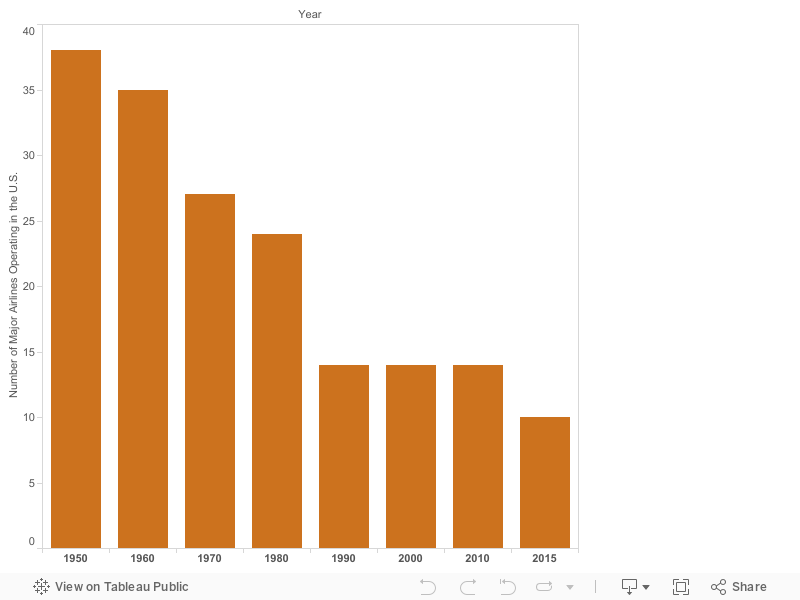

This merger was just another one in a series of high-profile mergers in the last decade. Today, there are four big carriers in the U.S. (America, Delta, Southwest, and United) that according to the Government Accountability Office carry more than 80% of domestic passengers. Each of these four large carriers all went through a recent merger: American with US Airways, Delta with Northwest, Southwest with AirTran, and United with Continental. Together with some smaller airlines (Alaska, Frontier, Hawaiian, jetBlue, Spirit, and Virgin America), a total of 10 airlines comprise nearly all of the market in 2015. The figure below shows the long term decline in how many “major” airlines were operating in the beginning of each decade since 1950.

Table 1: Number of major airlines operating in the U.S. at the beginning of each decade (plus 2015). Source: Aviation Week – Things with Wings.

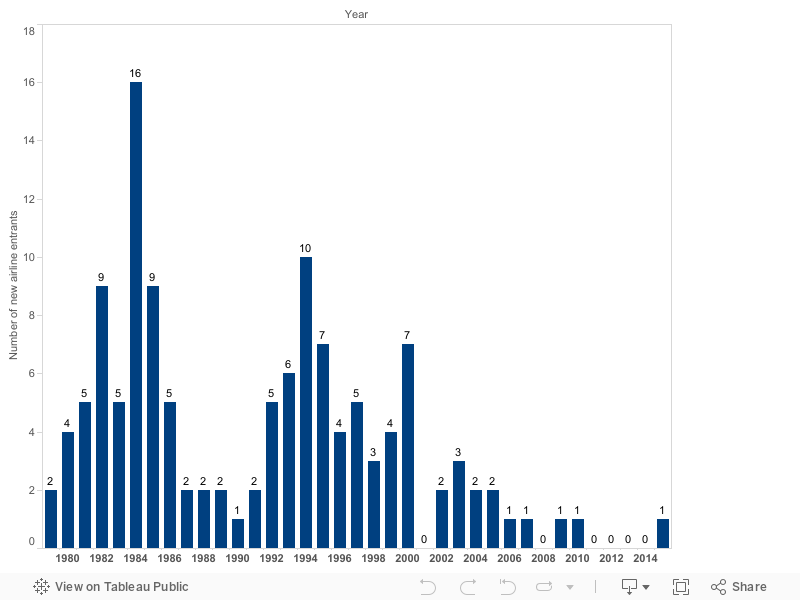

Deregulation of passenger airlines, which happened in 1978*, encouraged a flood of new competition to the market. In the two decades following deregulation more than 100 new airlines were started. Most of these disappeared quickly, either by merging with larger airlines or by bankruptcy – between 1979 and 2012 there were 194 airline bankruptcies, although many of those resulted in restructuring, not the end of the airline. Since 2001, the pace of new entries into the market has declined steeply (see figure below), and only one major airline, Virgin America, has entered the market. The most recent airline entrant, occurring earlier this year, is the third incarnation of Eastern Airlines, which currently is a charter-only airline.

*Number of airlines operating at deregulation: 32

Table 2: Number of new airline entrants per year. Source: Jordan, A. (2005). “Airline Entry Following US Deregulation: The Definitive List of Startup Passenger Airlines, 1979–2003” and Eno Center for Transportation internal research.

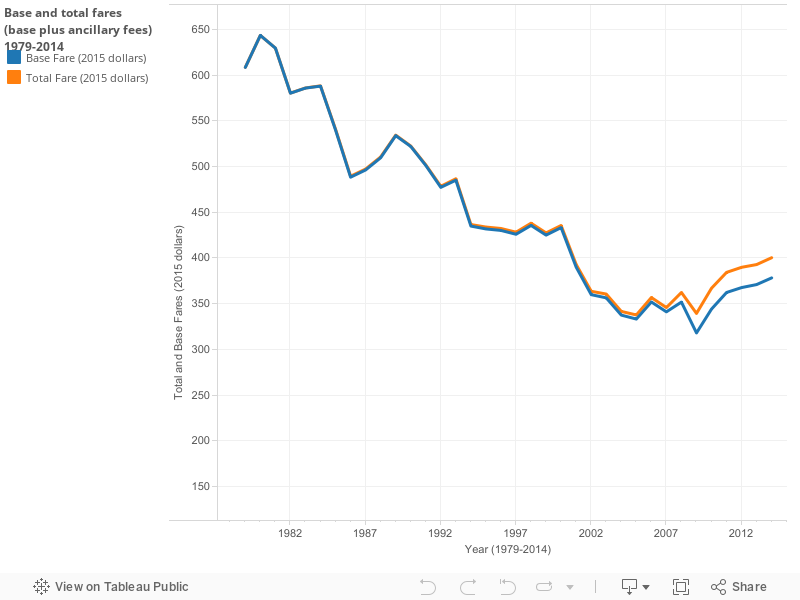

Despite multiple bankruptcies, deregulation has brought a significant reduction in air fares. In real terms overall fares have dropped from the pre-deregulation levels of the late 1970s (see figure below). While it is true that ancillary fees like baggage and change fees have increased and are a growing source of airline revenue, the fact is that ancillary revenues still only represent around 6% (or $25) of the total fare that passengers pay. In recent years airfares have rebounded from their lowest, inflation-adjusted point in 2005 and they still are lower than the long term average.

Table 3: Base and total (base plus ancillary fees) fares (1979-2014). Source: Airlines for America.

The effect of the industry consolidation, highlighted by the recent American-US Airways merger, has yet to be seen. Concerns from consumer groups include the potential for increasing fares and access/ service to smaller and medium-sized regions. While fare data is readily available and comparable with previous years, measuring access and service to small communities is more complex. While the number of direct flights have been cut in some cities, namely those that were hubs for airlines in the past, service to bigger airports has increased greatly (airports like San Francisco or Atlanta have around 200 direct domestic destinations). While it is true that a direct flight is usually preferable, for now at least most small communities kept the service to at least one of these major hubs, thus having access to many destinations.

How this has affected their ability to maintain business will require further examination.