Shuster Introduces His Infrastructure Bill

July 23, 2018

This evening, House Transportation and Infrastructure chairman Bill Shuster (R-PA) is releasing the text of his own legislative proposal to increase the quality and stability of U.S. surface transportation and water infrastructure.

The text of the draft bill can be viewed here.

In a statement, Shuster said:

“The 2016 presidential campaign shined a spotlight on America’s crumbling infrastructure. Since election day, the American people have waited for action by their federal elected representatives, and I am just as frustrated as they are that we have yet to seriously consider a responsible, thoughtful proposal. That is why I have released a discussion draft that reflects input from Members on both sides of the aisle, as well as a broad group of infrastructure stakeholders interested in building a 21st century infrastructure for our country.

“This discussion draft does not represent a complete and final infrastructure bill. It is meant to reignite discussions amongst my colleagues, and I urge all Members to be open-minded and willing to work together in considering real solutions that will give America the modern day infrastructure it needs.

“Over the coming weeks and months, I look forward to additional input from my Republican and Democratic colleagues in order to prepare a bill for congressional consideration.”

The draft bill has no title, and no cosponsors. Though Shuster did have initial conversations with Democrats on his committee, in the end there was no bipartisan agreement on the entire package. (T&I ranking minority member Peter DeFazio (D-OR) told reporters that he could not go along with the expedited project delivery provisions in the bill, and that four months before an election was a bad time to be talking about a gas tax increase.) Shuster is not actually introducing the bill in the House, which precludes any actual cosponsorship (and also precludes sending the bill to the Ways and Means Committee).

Highlights of the Shuster bill include:

- A package of motor fuel tax increases, and some new taxes on other highway and transit system users not currently taxed, that would raise at least $284 billion in new gross revenues for the federal Highway Trust Fund over the next ten years, averting future Trust Fund defaults and allowing significant highway spending above baseline.

- A new blue-ribbon commission to recommend future long-term Trust Fund solvency proposals that would get an automatic up or down vote in Congress with no amendments or filibusters.

- A one-year “clean” extension of the FAST Act to give Congress time for the blue-ribbon panel to report.

- Permanent statutory authorization for the grant program now known as BUILD and formerly known as TIGER.

- Project delivery reforms along the lines of those sought by the Trump Administration.

A brief overview of the bill follows.

Title I – Highway Trust Fund solvency.

Title I of the Shuster bill deals with the solvency of the Highway Trust Fund, which has required $144 billion in extra deposits from the general fund of the Treasury over the last decade because receipts from excise taxes on highway users have not kept pace with Trust Fund spending.

The Shuster bill addresses HTF solvency in three areas – immediate increases in existing HTF excise taxes, broadening the tax base with new excise taxes on classes of users receiving HTF funding, and long-term HTF restructuring.

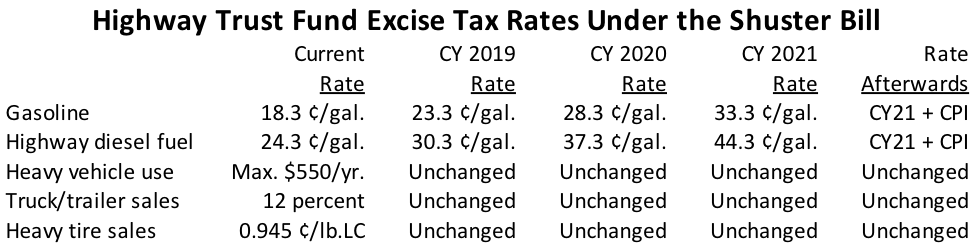

Increasing existing excise taxes. Subtitle C of title I of the Shuster bill would increase the existing federal gasoline excise tax by 15 cents per gallon over three years and would increase the existing highway diesel fuel excise tax by 20 cents per gallon over the same time period. The existing tax rates on tractor-trailer sales, heavy truck tire sales, and heavy truck use would be left unchanged, but since almost all highway diesel use is by the trucking industry, this is the justification for the higher increase in the diesel fuel rate.

After calendar year 2021, the fuel taxes would be increased every year by the annual rate of inflation (CPI). All of the motor fuel tax increases would be split 80-20 between the Highway Account and the Mass Transit Account.

The Shuster bill would extend those taxes, currently scheduled to expire in October 2022, through October 2028, and would extend expenditure authority from the Trust Fund itself, which is currently expiring in October 2020, only through October 2021 (pursuant to a one-year FAST Act extension later in the bill).

Broaden the HTF tax base. Subtitle B of title I of the Shuster bill would levy new or increased federal excise taxes on classes of highway and transit system users who currently pay nothing into the Trust Fund or who pay reduced rates.

- Mass transit buses. Sections 6421 and 6427 of the Internal Revenue Code currently provides that buses engaged in “passenger land transportation available to the general public” are can get refunds of the gasoline (6421) and diesel (6427) taxes. (The current rules are in IRS Publication 510.) Section 111 of the Shuster bill would repeal this tax break for transit buses.

- Commuter rail. At present, railroads are exempt from the HTF excise taxes on the diesel fuel burned by their locomotives. (Once upon a time, all railroads were subject to the 4.3 cent per gallon deficit-reduction diesel fuel tax levied by the 1993 Clinton budget law, but that eventually got repealed.) Section 112 of the Shuster bill would tax the diesel fuel used by passenger trains, if the trains are part of a public transportation system receiving HTF mass transit aid under section 5307 and 5337 of title 49 U.S.C., at 4.3 cents per gallon.

- Electric vehicle batteries. Section 113 of the Shuster bill would levy a new 10 percent sales tax on the batteries used in electric vehicles. For new EVs, the tax is 10 percent of “the price for which the motor vehicle was sold as is allocable to such battery.”

- Bicycle tires. Section 114 of the Shuster bill would levy a new 10 percent sales tax on each bicycle tire of at least a 26 inch inflated outside diameter (presumably so as not to tax children’s bikes and trikes which won’t be using public roads). As with the EVs, in the case of a new bike, the tax is 10 percent of the price of the bike as was allocable to the tire. (Eno’s Alice Grossman has separate analysis of a bike tire tax here.)

The new HTF taxes take effect on January 1, 2019. All of the new revenue increases would be split 80-20 between the Highway Account and the Mass Transit Account.

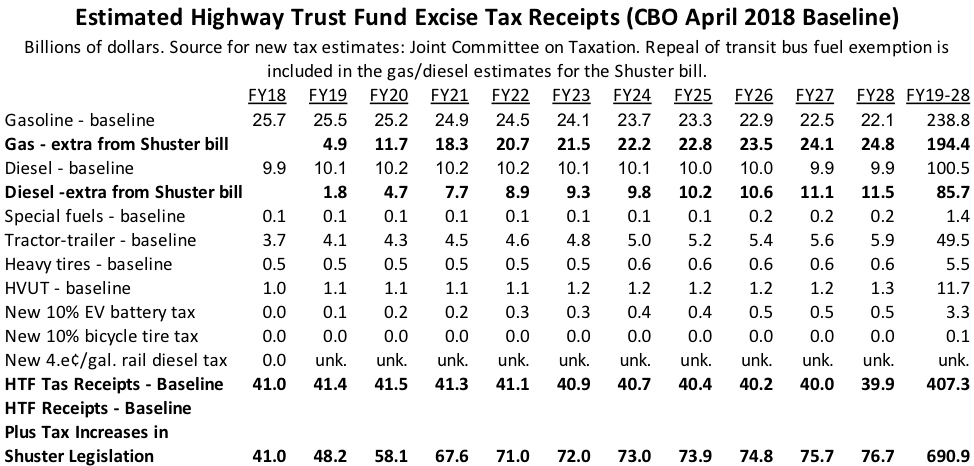

The Congressional Budget Office’s latest revenue baseline for the HTF, released in April 2018, predicted $407 billion in excise tax receipts over the ten-year 2019-2028 period. The Joint Committee on Taxation gave Shuster’s office a preliminary estimate of the additional revenues raised for the HTF from the legislation, and the increased moneys would total at least $284 billion – $194 billion from increased gasoline taxes, $86 billion from increased diesel taxes, $3.3 billion from the new EV tax, and almost $150 million from the bicycle tire tax. (JCT did not have time to calculate the commuter rail diesel fuel tax.)

At a minimum, even without the new commuter rail diesel tax, the tax increases in the Shuster bill would be enough to keep both accounts of the Trust Fund solvent for at least a decade under the baseline spending and tax projections issued by the Congressional Budget Office in April 2018. In the case of the Highway Account, the tax increases would allow significant spending growth significantly above baseline after the expiration of the FAST Act in 2020 – about $100 billion in total outlays above baseline could be supported over 2019-2028, if phased in properly. In the case of the Mass Transit Account, which is currently overspending its revenues at a far greater ratio than is the Highway Account, the new taxes would allow for slight spending over FAST Act rates (maybe $12 billion in outlays over 10 years).

Future HTF sustainability. Subtitle A of title I of the Shuster bill contains two provisions designed to put the Highway Trust Fund on a path to long-term sustainability. The first of these establishes yet another blue-ribbon panel, the “Highway Trust Fund Commission,” with 5 members appointed by USDOT, 5 by the House, and 5 by the Senate, the latter two in 3 majority to 2 minority ratios.

The Commission’s brief is to identify surface transportation system needs, determine necessary HTF revenue levels to meet those needs, evaluate revenue sources, and “anything else the Commission considers appropriate.” The Commission must report by January 15, 2021, and its report must include recommended legislative language to achieve the goals of the report. The only restriction is that the report “may not include a recommendation or proposed legislation to achieve long-term solvency of the Highway Trust Fund, in whole or in part, by enacting a Federal excise tax on gasoline or diesel fuel.” (Since a significant gas/diesel tax is included in the underlying Shuster bill, the presumed thought is that another gas tax increase after that would be overkill.)

However, unlike the previous blue-ribbon panels that were set up to recommend policies for the future of the HTF, this one comes with legislative “fast track” authority for the consideration of the Commission’s recommendations. Once the Commission files its report, the bill calls for a member to introduce it in each chamber, and the bill won’t be referred to committee – instead, it will be placed on the calendar of each chamber. 30 days after introduction, motions to bring up the bill in each chamber will be privileged (which means no filibuster in the Senate), and debate will be time-limited, and no amendments will be in order. If the President vetoes the bill, a vote to override the veto is not subject to filibuster in the Senate.

There are some inevitable loopholes in this language (especially in the House, where it is a commonly established precedent that the Rules Committee has the power to overturn legislative fast track provisions at any time), and the bill is a little vague on what happens if the majority leader in each chamber declines to pick a member to introduce the Commission bill, but the intent of the provision is to give the recommendations of the panel a real shot at bypassing legislative gridlock and becoming law.

The other provision in subtitle A is a direction to USDOT to establish a pilot program for a national per-mile user fee in section 102 of the bill. The two-year pilot program is funded by $15 million in contract authority.

Title II – Infrastructure investment.

FAST Act extension. Title II of the Shuster bill contains a one-year “clean” extension of the FAST Act (sec. 202), through fiscal year 2021, with all programs funded at their FY 2020 rates. It also repeals the $7.6 billion rescission of highway contract authority scheduled by the FAST Act to take place on July 1, 2020 (sec. 203).

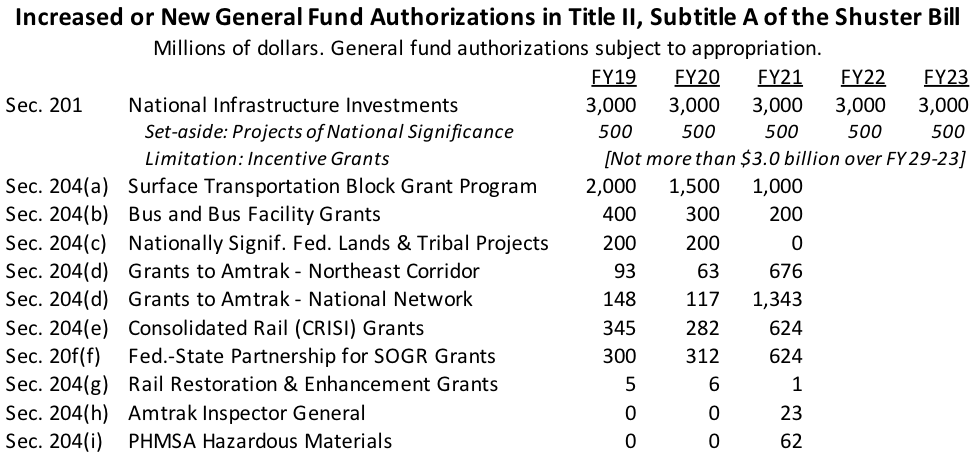

General fund authorizations. Since the enactment of the February 2018 bipartisan budget agreement, the Appropriations Committees have been pouring general fund money into surface transportation programs far in excess of authorized amounts. The Shuster bill in section 204 increases general fund authorizations for these programs in 2019 and 2020 above the original FAST Act levels to reflect what the appropriators have been doing and also adds higher FY 2021 authorizations for these programs to reflect the overall one-year extension.

The Shuster bill in section 201 also authorizes the never-before-authorized TIGER program (now called BUILD by the Trump Administration and always formally titled National Infrastructure Investments). Section 201 of the Shuster bill would authorize a NII program at up to $3 billion per year of general fund appropriations, with permanent statutory language that largely replicates what has been in the annual appropriations bills since 2010. Minimum grant sizes of $25 million and maximum federal share of 80 percent (except for rural projects where the federal share is higher), 30 percent minimum set aside for rural projects.

The authorization contains a few nods to the Trump infrastructure plan – it makes “transformative transportation projects” eligible for NII grants and also makes something called “incentive grants” eligible, but it defines the latter as a grant to an otherwise eligible applicant “that owns an infrastructure asset and has leased such asset to a private sector entity.” Such “incentive grants” cannot exceed 15 percent of the assessed value of the leased asset, and such grants are limited to no more than 15 percent of the NII total during the FY 2019-2022 period of the five-year NII authorization.

Section 201 of the Shuster bill also sets aside $500 million per year of the NII money for “projects of national significance,” which appear to be a way to circumvent the Congressional earmark bank. The bill requires DOT to submit reports to Congress each year identifying projects of national significance (to be suggested to DOT by potential project sponsors via an annual RFP). The bill authorizes Congress to appropriate money for projects in the annual reports if “such project has been authorized by an Act of Congress.” This seems designed to get authorizers and appropriators to work together to take some discretion in picking projects away from USDOT and vested back in Congress without actually violating the earmark ban.

The additional general fund authorizations are shown below.

INFRA grants. Section 205 of the Shuster bill requires DOT to send Congress annual lists of all the INFRA grant applicants that did not receive grants and sets aside a total of $200 million in contract authority over the three-year 2019-2021 period in INFRA grant money that can only go to unsuccessful prior-year applicants that were in such DOT reports and which are also allocated by an Act of Congress. (Another attempt to get around the earmark ban by making the Administration request individual projects.)

Water resources. Section 211 of the Shuster bill extends the WIFIA loan program at the EPA through 2024 at an appropriation level of $50 million of credit subsidy cost per year. It also reduces the number of rating agency opinions needed for a project from two to one and changes WIFIA debt subordination rules. Subtitle B of title II of the Shuster bill also contains a few program funding authorizations cherry-picked from the pending Water Resources Development Act, as well as a provision in section 216 that increases the funding authorizations for the State Revolving Funds under the Clean Water Act to reflect the extra money that the Appropriations Committees have been giving the programs.

Section 217 of the Shuster bill also contains an amendment that effectively exempts Harbor Maintenance Trust Fund appropriations from the Budget Control Act spending caps which currently constrain such funding. But the exemption only applies so far as the total HMTF appropriations in that year are do not exceed the total amount of HMTF tax receipts and interest in the fiscal year before the current year.

Title III – Innovative finance

Title III of the Shuster bill contains another authorization of general fund appropriations to reflect something the Appropriations Committees already did (money for RRIF loan subsidy authority) in section 301. Section 302 establishes a public-private partnership program for GSA building acquisition. Section 303 is an attempt to replicate one of the more innovative ideas in President Trump’s infrastructure plan, a revolving fund for large federal real estate purchases to ease the pressure on the annual appropriations totals. Section 304 establishes a federal credit program for Coast Guard housing authorities.

Title IV – Project delivery

Section 401 of the Shuster bill amends 49 U.S.C. §116(f) to require the Build America Bureau (or whatever they are calling it now) to “ensure that a record of decision is issued for a specified project that requires approval by the Department not later than 2 years after the date on which a notice of intent is published” (“specified project” means any highway, mass transit, airport, port, rail or multimodal projects).

Section 402 of the Shuster bill amends 49 U.S.C. §304 to make categorial exclusion apply to basically all transportation projects instead of just multimodal projects and to add the Surface Transportation Board to the list of potential lead authorities or cooperating authorities.

Section 403 of the Shuster bill establishes a new USDOT pilot program “to assess the use of innovative practices in the environmental review process of a project.”

Section 404 of the Shuster bill clarifies section 401 of the Clean Water Act as to only apply to water quality standards in effect under section 303 of the Act.